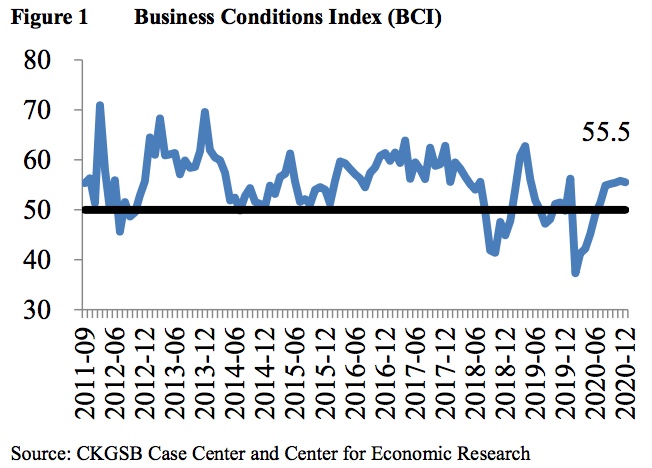

In December, the CKGSB Business Conditions Index (BCI) registered 55.5, a small fall in confidence on November’s figure of 55.8 (Figure 1).

The CKGSB BCI comprises four sub-indices: corporate sales, corporate profits, corporate financing environment and inventory levels. Three measure future prospects and one, the corporate financing index, measures the current climate. In December 2020, these sub-indices performed as follows:

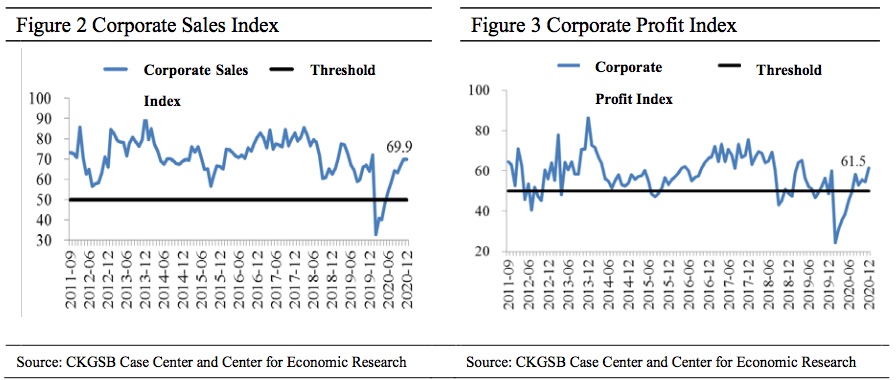

One rose and three fell this month. The corporate sales index fell minimally from 69.9 to 69.85 (Figure 2), and the corporate profit index rose from 54.5 to 61.5, on the positive side of the confidence threshold.

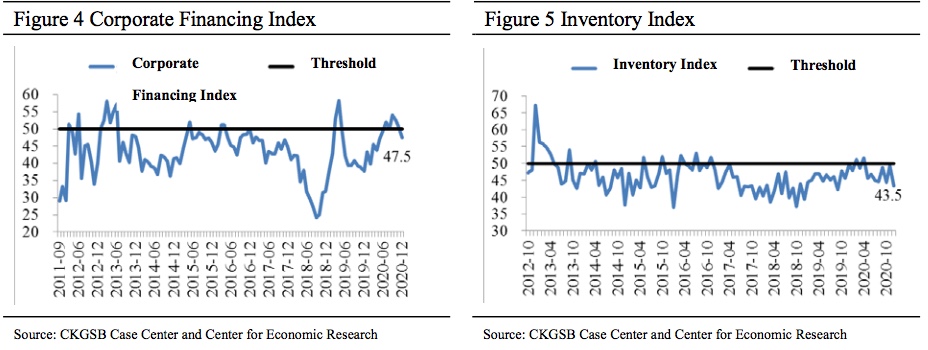

Corporate financing prospects were revised downwards, with the index falling back somewhat from 50.6 to 47.4 (Figure 4), taking it below the confidence threshold. The inventory index fell back to 43.5 from 49.3 (Figure 5). These two indicies have been problematic since the start of our survey in 2012, showing a persistently negative outlook.

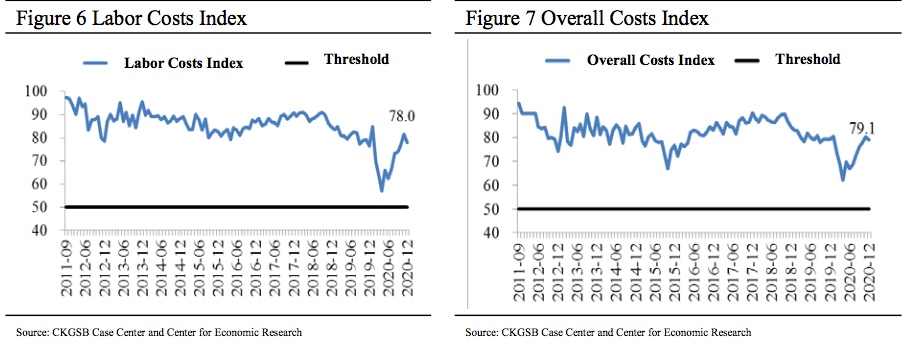

Aside from the main BCI, we also forecast costs, prices, investment and recruitment demand over the next six months. We begin with costs:

This month’s labor cost forecast fell from 81.4 to 78.0. The overall cost forecast fell from 80.3 to 79.1. See Figures 6 and 7 for more.

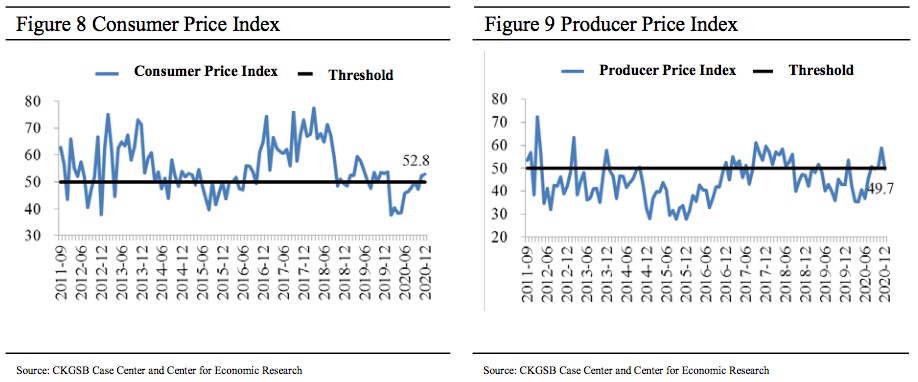

Turning to prices, the consumer price forecast rose minimally from 52.1 to 52.8 (Figure 8) while the producer price index fell back from 58.8 to 49.7 (Figure 9), wiping out last month’s gains. This sees consumer price prospects move higher than the producer price index.

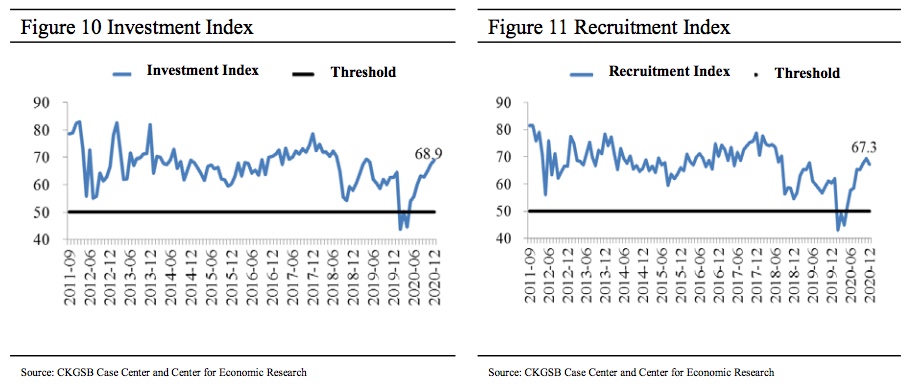

We now turn to investment and recruitment. These two indices have been consistently at the more confident end of the scale since the BCI began. In recent months however, both have weakened, especially recruitment, but this month one rose and one fell, with investment conditions rising from 67.4 to 68.9 (Figure 10), and recruitment prospects lower at 67.3 from last month’s 69.3 (Figure 11).

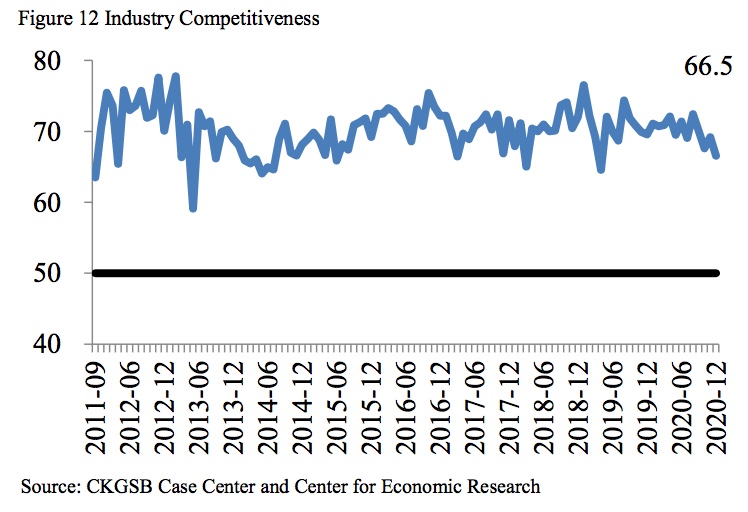

Finally, we include an index recording our sample’s relative strength in the marketplace. Figure 12 shows surveyed companies’ self-reported competitiveness compared with peers. As our sample mostly comprises of excellent private firms headed by CKGSB alumni, their competitiveness is higher than average (50 points) in their respective industries. This suggests that Chinese industry as a whole is facing a harder time in the near future than the BCI cohort.